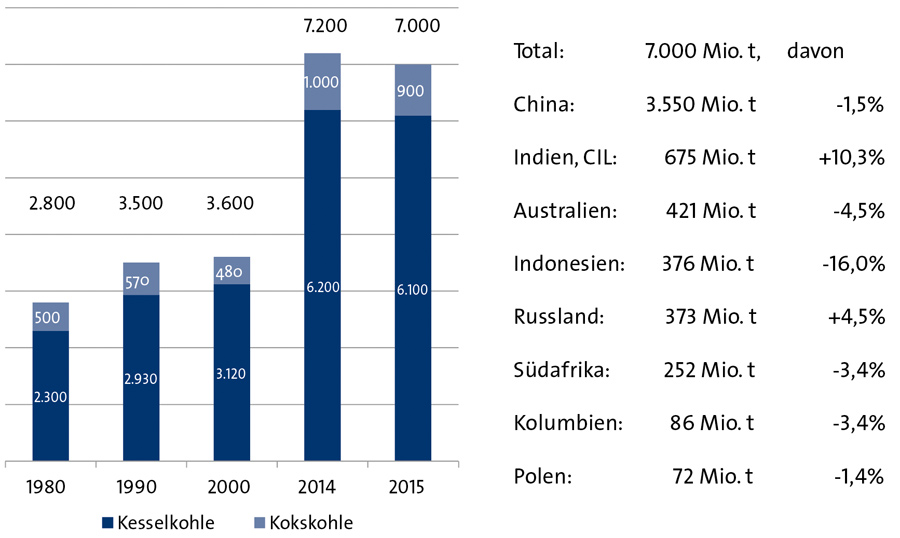

In August 2016, the German Coal Importer Association (VDKi), Hamburg, presented its annual report which, among other things, addressed the development of global coal markets (Figure 1). According to the report, coal mining fell worldwide by almost 3 % to 7.0 bn t in 2015. At 10 %, the drop in coking coal was significantly sharper than the 1.6 % drop in steam coal. This was caused by the general global economic trend and the declining demand for steel in China in particular. American producers of coking and steam coal have been hit particularly severely. A hard US dollar, the steel crisis and shale gas made for an explosive mixture for almost all producers. Except for Consol Energy, all American companies were dropped from the Dow Jones US Coal Index and each in turn filed an application for creditor protection under Chapter 11.

Fig. 1. Global coal production in million tons. // Bild 1. Globale Steinkohlenproduktion in Mio. t. Quelle/Source: VDKi

Chinese mining declined by 1.5 %. Chinese imports tumbled by 32 % and swept Indonesian and Australian production along with it. The 18 % drop in Indonesia was particularly extreme, because poorer quality coal was even more severely affected by Chinese regulation. Australia was able to compensate for the declining coking coal supplies to some extent thanks to additional supplies of high-quality steam coal.

According to the VDKi, India has a key role to play in the further development of the market. In 2015, the country saw production increase by 10 % compared with the previous year. If it could throw off the shackles of bureaucracy and overcome its logistical issues, the country’s level of self-sufficiency would increase again. Failing that, the growth in demand would make room for even more coal imports.

1,104 mt of seaborne trade comes from 833 mt of steam coal and 271 mt of coking coal. Australia regained its position from Indonesia at the top of the list of the biggest coal exporters in 2015, with a total of 387 mt – of which 202 mt and 185 mt were steam coal and coking coal respectively. Russia maintained its position, while Colombia and South Africa overtook the USA. Indonesia sends 97 % of its production to Asia. Australia places a similarly strong emphasis on Asia, which receives 87 % of Australian seaborne trade. Owing to their geographic location, Russia, Canada and the USA are able to supply both markets and trade is shifting increasingly towards Asia. Colombia (still) sends the majority of its exports to Europe.

In the Atlantic market, demand for steam coal in 2015 increased by 0.5 % to 217 mt. By contrast, demand in the Pacific market fell by 7 % to 616 mt. The Atlantic market’s share of the overall market is 26 %.

Chinese imports fell by 32 % to 156 mt. A slight increase of 1 mt in its imports to 216 mt made India the largest importer. Japan also upped its imports only slightly to 191 mt.

Steam coal prices continued to fall in 2015. This deterioration came to an end for the majority of countries in early 2016, but it is still too early to speak of it bottoming out, according to the VDKi. Whether the market shakeout in the interim was sufficient for this or not cannot yet be determined. The FOB prices on the US East Coast fell in January 2016 compared with the same month the previous year by 14 US$/t to 43 US$/t and were at 44 US$/t in June 2016.

The Pacific steam coal market showed

the same trend. At Richards Bay, the FOB price fell from 61 US$/t to 51 US$/t in 2015. By June 2016, it had risen back up to 58 US$/t.

The Russian Baltic coast FOB prices dropped in January by 13 US$/t compared with the same month the previous year; prices even fell for exports to Asia by 17 US$/t. When calculated in roubles, however, revenues did increase slightly – an exceptional situation resulting from the particularly weak currency.

Trade on the global seaborne coking coal market experienced a much sharper decline than global steel production, namely by 12.3 %. The market shares of individual countries have also seen a marked shift. Australia’s market share rose by eight percentage points up to 68 %. The USA’s share dropped by three percentage points down to 14 %. Although Russia was able to double its market share the previous year, it almost halved in 2015 – falling from 11 % to 6 %.

The downward trend in coking coal prices continued in 2015. The price of Australian prime hard coking coal suffered a serious slump from 114 US$/t in January 2015 to 77 US$/t in January 2016 (-32 %). Up to May 2015, the price stabilised around 94 US$/t. It responded to the trends in ore prices and was not influenced by the development of steam coal prices. By June 2016, it had risen to 89 US$/t.

At the beginning of 2016, the increase in capacity of the bulk carrier fleet almost came to a standstill. This was caused by an increase in the number of ships sold for scrap. As a result, the price of scrap almost halved the previous year. Owing to the poor market climate, it can be assumed that the amount of scrap will continue to increase and the ships being scrapped will be younger and younger.

For capesize ships heading to Rotterdam with a capacity of 150,000 dwt, the freight rates at the beginning of 2015 amounted to 5.90 US$/t from e. g. Colombia. The freight rates continued to increase up to the middle of the year but slumped again at the end of the year and were only 5.20 US$/t at the beginning of 2016. The current freight rates from Colombia have remained at this start-of-year figure.

The real gross domestic product (GDP) grew by 3 % globally in 2015. Two countries in particular helped to increase this average considerably. In China, real growth was 6.9 %; in India 7.4 %. According to the OECD’s Interim Economic Outlook from February 2016, only India is set to continue to grow at the same rate, whereas Chinese growth will lessen, albeit remaining above 6 %.

In future, development will be shaped primarily by India and Southeast Asia. Despite the growing contribution of renewable energies, coal will remain one of the mainstays of energy supply. The predominant driving force behind this is the construction of new coal-fired power stations in national economies with a backlog of economic demand.

The International Energy Agency’s (IEA) Medium Term Outlook anticipates that demand for coal, including lignite, will fall in the OECD area up to 2020 – and this fall will be consistent in all OECD countries. By contrast, demand for coal in OECD non-member countries will grow.

The IEA also anticipates that seaborne trade in Asia will see a marked increase once again, from 954 mt in 2016 to 1,128 mt in 2020, whereas it will see a decline in Europe and North America. Overall, this would result in growth of 1.2 bn t in 2016 to 1.35 bn t in 2020. This growing demand would enable better use of capacity. In fact, additional export capacity would need to be made available for the future. These findings are a marked contrast to the general perception of the coal industry and campaigns that call for the finance sector to be phased out of fossil fuels.

According to the VDKi, the development of the global coking coal market is influenced by excess capacity in China. Initial recovery of prices for ores and coking coal at the beginning of 2016 is still no indication that the crisis is over. In reality, the prices should have given way once more. Given that structural improvements in China have only just begun, it is still too early to be able to assess the effectiveness of the protective measures put in place by the European Union.

One sign of recovery in the sector may be, according to the VDKi, the increase in capacity use in global steel production from 65 % in December of the previous year to 71.5 % in April. Whether or not this is an indication of the much anticipated light at the end of the tunnel remains to be seen and depends on economic development around the globe. (VDKi/Si.)