Grounds for coal policy decisions

The ultimate goal pursued by the energy transition in Germany is more than ambitious: the transformation to climate neutrality of the entire German economy and society by 2045. At the same time, there has not been any wavering from the decision to phase out the use of nuclear power in Germany, which was made in 2011 after the Fukushima accident and which provided for the gradual shutdown of all German nuclear power plants by the end of 2022. Realisation of this decision has continued on schedule so that as of 2022, only three out of the once seventeen nuclear power plants in Germany were still in operation. The objective is the complete conversion of the energy supply in Germany to renewable energies and green hydrogen obtained using green electricity and away from nuclear and fossil fuels. The latter also means phasing out the use of oil and natural gas. But a specific plan has been set only for the reduction and cessation of coal-fired power generation by no later than 2038. Even the coalition agreement of the German government of 2017 (at that time: SPD and CDU/CSU) referred to such a plan, and the “Commission for Growth, Structural Change and Employment (KWSB)” was instructed in June 2018 to work out the details. The end of coal-fired power generation also means – and this was clear as a consequence of the close economic interdependence of opencast lignite mines and power plants – the end of domestic lignite mining in Germany. The phase-out of the German coal industry had almost been completed even at that time; operations in the last two German coal mines (Prosper-Haniel in the Ruhr coalfield and Ibbenbüren) ceased at the end of 2018 in accordance with the coal policy agreements of 2007 and 2011 (deletion of the so-called revision clause) for the socially acceptable termination of coal subsidies by 2018.

The Coal Commission had the task of determining the broadest possible social consensus on a feasible path for the exit from coal-fired power generation in Germany in line with energy and climate policies and the associated structural transformation in the coal regions. Its membership comprised various actors from politics, business, trade unions, environmental associations and the affected regions and German states. Incidentally, the coal industry itself was not involved; it was merely consulted. On 31st January 2019, the Coal Commission concluded its work and presented its final report. It recommended the gradual phase-out of coal-fired power generation by no later than 2038 or possibly as early as 2035, subject to certain general energy, regional and social-political conditions: future assurance that a secure and affordable electricity supply would remain available from the accelerated expansion of wind power and photovoltaics (PV) in conjunction with the simultaneous construction of highly efficient natural gas-fired power plants and the switch from coal to natural gas in CHP plants and district heating systems promoted by a “natural gas investment framework” along with compensation for rising electricity prices for private and commercial electricity consumers; the latter would require the creation of appropriate programmes. Furthermore, the Coal Commission issued various recommendations for parallel actions to assure the successful management of the economic structural change in the affected regions.

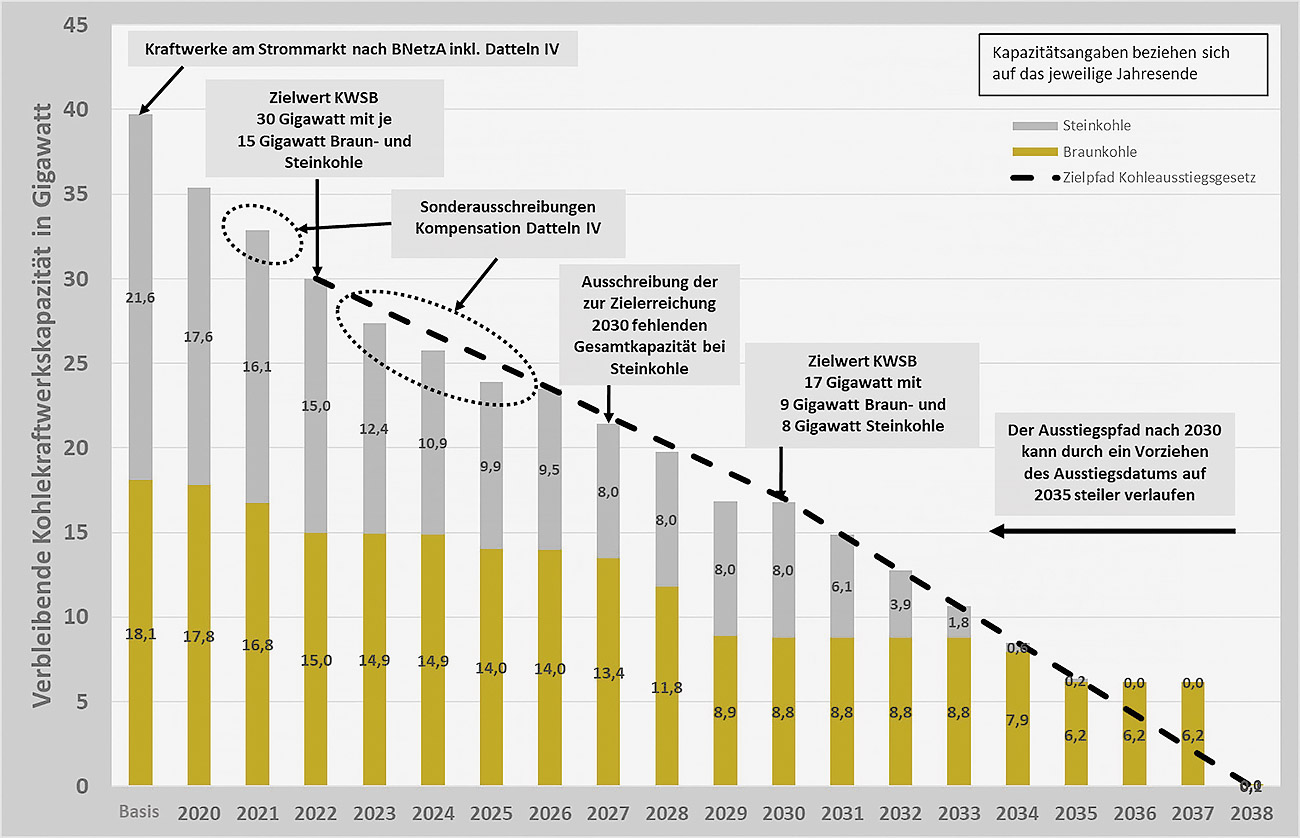

The German government at the time adopted by and large the recommendations of the Coal Commission, including the exit date, cast them in the required formats and adopted several packages of legislation based on them. On 3rd July 2020, the Coal Phase-Out Act (Act to Reduce and End Coal-fired Power Generation and to Amend Other Laws) was passed by the Bundestag. On 14th August 2020, the Act for the Strengthening of the Structures of Coal Regions was passed in association with the Coal Regions Investment Act as its “stem act”; it provides specific structural funding for coal regions until 2038 in the form of mainly public investments by the federal government and the German states, i. e. no grants for private investments, with total volumes of 40 bn € for the German lignite regions and of slightly more than 1 bn € for structurally weak municipalities at the locations of coal-fired power plants, including five municipalities in the Ruhr area and two in Saarland, i.e. in regions where coal mining had been shut down, but for which no other special structural funding is granted. These measures are supplemented by additional subsidisation opportunities within the scope of the general regional funding of the German government/German states joint task “Improvement of the Regional Economic Structure” (GRW) and the EU Structural Funds, including the Just Transition Mechanism set up for the “Coal Transition” in the member states. As of the end of 2021, projects based on these actions with a value of more than 19 bn € had been launched in the coal regions. Prerequisite for their realisation is the implementation of the energy industry adaptation path required by the Coal Phase-Out Act, which (in addition to a ban on the construction of new coal-fired power plants) foresees as a first step the reduction of domestic coal-fired power capacities from 42.5 GW in 2017 to 30 GW by the end of 2022; as of the moment, this process is on schedule. The second step requires the reduction of these coal capacities to a total of 17 GW (9 GW lignite and 8 GW hard coal) by 2030, followed by their reduction to zero by 2038 or, depending on the review scheduled for this purpose in the second phase in 2026, by 2035 – completely terminating coal-fired power generation in Germany.

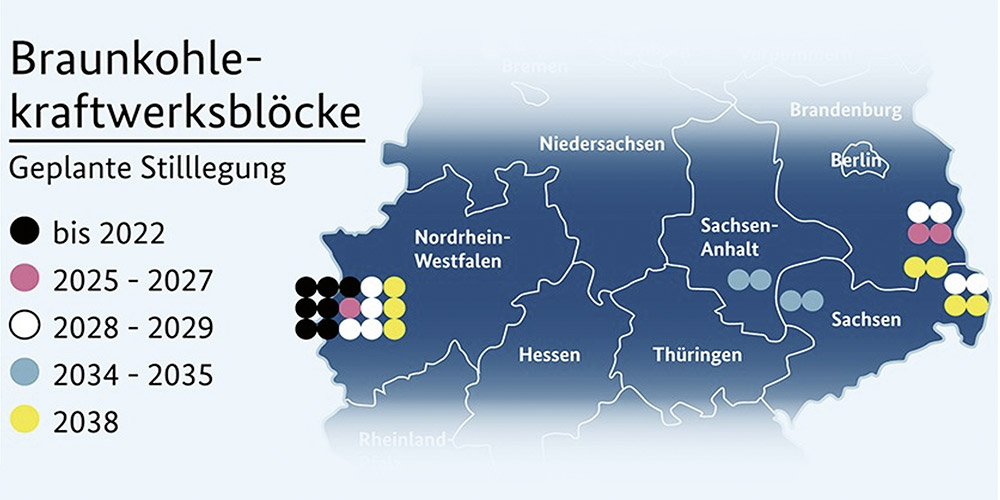

Besides the statutory regulations, a public-law contract governing the shutdown of lignite-fired power plants and opencast mines has been concluded; it specifies a timetable for the shutdown of each individual operation as well as compensation payments dependent on the shutdown dates to the power plant operators and additional measures supporting implementation, including recultivation. According to this plan, the first closures – three lignite-fired power plant units – will occur exclusively in the Rhenish coalfield by 2022. Five further shutdowns in the Rhenish coalfield and six closures in the Lusatian coalfield have been scheduled in the period between 2025 and 2029. Finally, the Central German coalfield and its four plants will be closed down completely in 2034/2035 before the remaining three plants in the Rhenish and four plants in the Lusatian coalfield and with them the remaining domestic lignite mining industry are shut down in 2038 or possibly as early as 2035.

In contrast, a degressive tender procedure for shutdown premiums for hard coal-fired power plants starting in 2020 was defined to assure shutdown rates as close to schedule as possible. As of 2028 and later, the remaining German hard coal-fired power plants will be shut down by regulatory orders without compensation, and the reduction of domestic hard coal-fired power generation will continue on schedule until it ends completely by 2035 (Figure 1).

Fig. 1. Legally scheduled exit path for coal-fired power generation. // Bild 1. Gesetzlich vorgesehener Ausstiegpfad für die Kohleverstromung. Source/Quelle: BMUV

In support of these state-initiated shutdown processes, the German government has committed to granting an adjustment allowance to finance early retirement schemes for older workers in the coal industry similar to the successful programme for the socially acceptable adjustment of the coal mining industry and that is now being extended to employees in the lignite mining industry and in the lignite- and hard coal-fired power plants. The Coal Phase-Out Act contains a climate policy provision allowing the legal cancellation of the CO2 certificates that become available as a consequence of the closures; the measure serves to avoid counterproductive effects in the EU Emissions Trading System. (1)

In its coalition agreement “Dare More Progress” concluded at the end of November 2021, the newly elected German government of the “traffic light coalition” (SPD, Greens, FDP) states that compliance with national climate protection targets and the intended tightening of the EU emission trading “will require accelerated phase-out of coal-fired power generation. Ideally, this will have been achieved by 2030.” The exit date for coal-fired power generation, which had been set by law only one year earlier, would have to be brought forward by five to eight years. The structural and social policy support for the affected regions and the people affected by coal mining would remain unchanged, however; the related measures would merely be brought forward, adapted where necessary and supplemented. “No one will be left to fend for himself”, emphasises the coalition agreement. The possibility of “establishing a foundation or company for the organisation of the dismantling of coal-fired power generation and renaturation” should also be considered. The accelerated exit from coal-fired power generation, according to the traffic light government at the end of 2021, will require the acceleration of a “massive expansion of renewable energies and the construction of modern natural gas-fired power plants so that the growing demand for electricity and energy over the coming years can be met at competitive prices.” According to the coalition agreement, this would be achieved by moving the review step scheduled for 2026 in the Coal Phase-Out Act forward to the end of 2022 at the latest, analogously to further provisions of the Act. The “natural gas-fired power plants that will remain necessary until security of supply is ensured by renewable energies” should also be built at existing power plant sites so that they can use the existing (grid) infrastructures and (regional) future prospects can be assured. Their construction will have to include the possible conversion to climate-neutral gases (H2-ready). “We will regularly review the security of supply and the rapid expansion of renewables. To this end, we will continue to develop the monitoring of the supply security of electricity and heat into a genuine stress test.” (2) According to the coalition agreement, coal-fired power plants should be converted to natural gas wherever possible at existing locations while at the same time the natural gas-fired power plants replacing coal-fired power generation and their infrastructure will be prepared for the production of hydrogen in the future. Moreover, the process of phasing out coal and its pace will be conditional on the security of electricity supply; a “genuine stress test” (i.e. the question of whether supply can be guaranteed even under extremely unfavourable conditions) should also be incorporated into the future monitoring of the supply.

According to § 55 of the Act on the Reduction and Termination of Coal-fired Power Generation (KVBG), the Federal Network Agency must as of 2021 regularly monitor and determine on an annual basis “whether to a sufficient degree of probability the safety and reliability of the electricity supply system is not endangered or disrupted to more than a minor extent by the measures pursuant to this Act. In doing so, it will give special consideration to the extent to which the hard coal-fired plants can continue to be available to the transmission system operators outside the market within the scope of the grid reserve for secure and reliable grid operation.” It was determined for 2021 that no such threat existed, provided that the other framework conditions did not change.

Pursuant to § 54, para. 1, KVBG, the German government must, by no later than 15 August of each of the years 2022, 2026, 2029 and 2032, review “on a scientific basis, including specified criteria and associated indicators, the impact of the reduction and termination of coal-fired power generation”, explicitly the impact on:

- the security of (power) supply;

- the number and capacity of plants converted from coal to natural gas;

- the maintenance of the heat supply;

- the electricity prices;

- the achievement of each of the target levels of the Act;

- the contribution to achievement of the associated national climate protection targets;

- raw materials, in particular gypsum, which are obtained in the course of coal-fired power generation; and

- in 2022, the review must also cover the social compatibility of the initiated coal phase-out.

In addition to further reviews by the German government itself, § 54, para. 4, KVBG requires the Federal Network Agency to “determine whether the existing natural gas supply grids are adequate to enable hard coal and lignite plants to convert to natural gas as an energy source” for the federal government’s review as of 2022 and later.

Pursuant to § 56 KVBG, the German government should, during the regular comprehensive reviews in 2026, 2029 and 2032, simultaneously review whether each of the milestones for the reduction and cessation of coal-fired power generation after 2030 can be brought forward three years and whether the date of 31st December 2035 for the final exit can be achieved.

Consideration of the latter provision makes it clear that the new objective of bringing forward the coal phase-out to 2030 stated in the coalition agreement would require an amendment of the KVBG and a fast decision and determination concerning the earlier exit date. In the following, the case for an amendment of the KVBG will also be made, but in the opposite direction: the reduction and termination of coal-fired power generation should be suspended for the time being and as soon as possible. There are valid reasons for taking this step because in the light of developments in 2022, the criteria set forth in the KVBG no longer justify a coal phase-out at this time.

Meanwhile, the federal government has allowed the legal deadline for the first audit report of 15 August 2022 to expire. (3) There are indications that the report will possibly be issued by the end of the year. No official reasons have been given for the delay. What is clear, however, is that the assumptions and prerequisites on which the coal phase-out was based have fundamentally changed in the meantime. The guiding idea of the Coal Phase-Out Act – the replacement of coal with natural gas as a backup for renewables in power generation – is no longer feasible.

New era in German energy policy – natural gas no longer reliable for the transition

Prior to the beginning of the coronavirus pandemic in 2020, world fossil fuel prices were at a relatively low level, global supply exceeded demand and international markets for coal or natural gas were evidently buyers’ markets. The prospect of worldwide decarbonisation manifested since the World Climate Conference 2015 in Paris and especially the “Green Deal” adopted in 2019 with the goal of climate neutrality in the EU by 2050 also promised in the long term a shift away from fossil energies, first and foremost from coal, and a turning towards electricity generation from renewable energies in conjunction with cross-sector electrification. These goals were also intended to strengthen the security of energy supply by successively reducing dependence on energy imports from politically uncertain supplier countries such as Russia or the OPEC states. It has often been overlooked, however – especially in the German energy debate – that this shift leads to new dependencies on hitherto non-energy critical raw materials such as lithium, nickel, cobalt or rare earths without which the green energy transition cannot be realised and for which the concentration of raw material deposits and production in only a few and/or politically unreliable countries is in some instances even more critical than is true of oil, natural gas, hard coal or even lignite. In addition, there are the risks and vulnerabilities of critical energy infrastructures such as gas pipelines or power lines that are not limited to political or technical factors, but include as well, e. g., terrorism or cyberattacks. (4)

With the outbreak of the pandemic or the in part drastic measures initiated to combat it, economies and trade collapsed worldwide and energy demand and prices fell almost globally. The developments caused a substantial reduction or shutdown of global production capacities and investments in the fossil energy sector such as the consolidation of shale oil and gas production in the USA or of tanker capacities for the maritime transport of oil and liquefied gas, all of which initially went virtually unnoticed in Germany. When economies began recovering at an unexpectedly rapid pace – in Asia as early as the end of 2020 and by spring 2021 in the rest of the world – energy demand, including demand for natural gas and LNG imports, rose sharply and exceeded available supply, leading to an initial shortage and price explosion, especially in the natural gas sector. In the EU, natural gas prices in September 2021 were as much as 600 % higher than one year earlier. “To this extent and until that time, the European natural gas crisis was initially above all a consequence of the imbalance between the higher global demand and the worldwide supply”; nevertheless, few in Germany (apart from expert circles) paid any attention to this or to the manipulative role of Russia in supplying natural gas to Europe such as the low filling of the natural gas storage facilities in the EU (some of which are operated directly by Gazprom) as also occurred in this country. (5)

The strong upward trend in CO2 prices in EU emission trading from about 30 €/t at the beginning of the year to almost 100 €/t towards the end of the year also contributed to the rise in natural gas prices and in coal and electricity prices, which also rose sharply in 2021. The decisive impetus behind this trend came from the new regulations for the fourth phase of the EU ETS, which went into effect in 2021, and the further tightening of the EU’s “Fit for 55” pact, which aims to achieve an EU-wide reduction in CO2 emissions of 55 % by 2030. The annual reduction rate in the EU ETS, which had achieved an overall reduction of more than 40 % by 2020 compared to 2005, has been raised further. This is yet another action aimed at encouraging the switch from coal to natural gas during the transition to a decarbonised energy system, but the initial effect is to drive up electricity and energy prices.

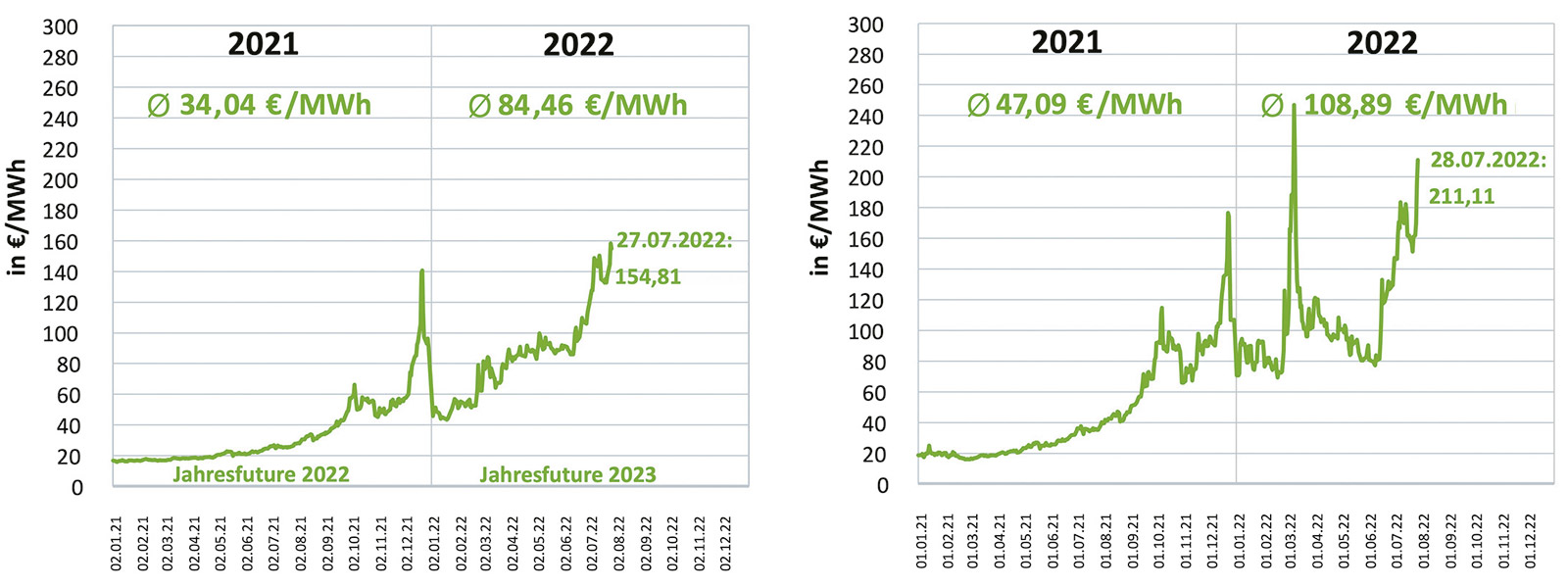

Russia’s military invasion of Ukraine on 24th February 2022 represented a “new era” in German security policy, as Chancellor Scholz declared shortly afterwards with broad approval in the German Bundestag. The issues of energy, especially natural gas supply security, are elements of this policy. As of 2021, Germany had become dependent on Russia for more than one-quarter of its primary energy supply; dependency on Russian natural gas at 55 % was even higher, and plans were to increase procurements once the Nord Stream 2 pipeline, which was nearing completion, was in operation: a cluster risk that was in contradiction to the long-established principle of a balanced, broadly diversified energy mix and that had been the subject of warnings from security experts as well as EU partners, the USA and Ukraine for some time. (6) The Kremlin’s decision to invade Ukraine and the subsequent war followed by the related sanctions imposed by the USA and NATO countries in response (including the suspension of the Nord Stream 2 project) have forced the EU countries (Germany in particular) to face unprecedented cuts and interruptions in Russian natural gas supplies, even the threat of a complete halt in deliveries, in addition to a dramatic deterioration in political and economic relations with Russia. Alternative import options – generally LNG (liquefied natural gas) transports from other continents as replacements for Russian pipeline natural gas – have as of this moment been developed solely to a relatively small extent and are labouring under the tense global natural gas market conditions. Persistent shortages and a further explosion in natural gas prices were and are to be expected (7), which in 2022 also triggered rapidly rising prices for electricity owing to the merit order effect on the electricity market (at the end of August 2022, e. g., the price on the EEX (Phelix baseload) reached 988 €/MWh, more than ten times the daily value in the previous year (85 €/MWh) (8)) and a serious energy crisis as well as a debate on electricity market reforms (Figures 2, 3).

Fig. 2. Wholesale prices for natural gas 2021/2022. // Bild 2. Großhandelspreise Erdgas 2021/2022. Source/Quelle: BDEW/AGEB 8/2022

Fig. 3. Development of electric power prices 2021/2022. // Bild 3. Strompreisentwicklung 2021/2022. Source/Quelle:EEX, entso-E

At the same time, the increased energy prices are regarded as the principle driver of overall economic inflation, which has reached a level similar to that following the first world oil price crisis in the 1970s and a record value for reunified Germany. It has been accompanied by major losses in consumer purchasing power and recessionary trends across all sectors, but especially in the entire energy-intensive economy, from chemicals, steel, metals, building materials, cement, glass and paper to fertiliser production or the automotive supply industry to the bakery trade and other food production and elsewhere.

The German government has implemented numerous measures in response to the energy crisis ranging from intensive trade policy efforts for LNG supply contracts, financial aid and accelerated permits for liquefied natural gas terminals in Germany and international solidarity agreements to the increase of national natural gas storage requirements and a nationalisation of the natural gas storage companies, the natural gas emergency plan and various related amendments of the Energy Security Act to aid programmes for energy consumers, the support of natural gas trading companies crippled by the crisis and the reduction of VAT for private natural gas customers to mitigate the impact. Such actions have been supplemented by energy-saving regulations and appeals – “take less time in the shower”, lower temperatures for heating private residences, 20 % less natural gas consumption, etc. Simultaneously, an acceleration package for the further expansion and prioritisation of wind and solar power plants in Germany has been launched.

A parallel action of the German government was the presentation of a bill for the Act for Standby Operation of Substitute Power Plants, adopted by the Bundestag in mid-July 2022, essentially a “natural gas replacement reserve” for the electricity market. Its provisions allow oil- and hard coal-fired power plants with a total capacity of 5.9 GW (4.3 GW for coal power plants) from the so-called grid reserve of the transmission system operators to be “allowed to return to the market” temporarily and under certain conditions, including for coal stockpiling, until spring 2023 with the aim of reducing natural gas-fired power generation and of preventing bottlenecks. The same provisions apply from October 2022 and until 1 March 2024 to 1.3 GW capacity of lignite-fired power plants in “security standby” and additional hard coal-fired power plants that were scheduled for closure in 2022 and 2023 in the plans for the coal phase-out. (9) However, these activations are voluntary and are not supposed to turn into permanent operation; moreover, their implementation has been sluggish.

It remains to be seen whether all these measures will be adequate to avert a natural gas supply emergency in the winter of 2022/2023, to avoid a longer-lasting natural gas and electricity supply crisis and to slow down noticeably the extreme increases in electricity and energy prices. Grave doubts are certainly justified. Aside from the exorbitant burdens and supply risks for private consumers, German industry in particular is caught in an “energy price trap” (Handelsblatt). The high natural gas and electricity prices translate de facto into serious competitive disadvantages for companies in Germany as a business location and encourage deindustrialisation, a process that has been underway in energy-intensive industry for some time, but is now intensifying and spreading markedly. Even before the current energy crisis, Germany had the highest industrial electricity prices among industrialised countries, and that was before adding the electricity tax. At just under 111 €/-MWh in mid-2022 (there were spikes of well over 300 €/MWh during the year), natural gas prices in the EU were twice as high as in Japan (equivalent to 55 €/MWh) and more than four times as high as in the USA (around 25 €/MWh). This spectacular gap will not be closed even if the natural gas market drops to a lower level, a development that is unimaginable at present because of the high delivery costs for LNG. In the long term, however, Germany’s competitiveness as an industrial location is at jeopardy – with all the related economic and social consequences. (10)

The reliance on natural gas as a bridge on the journey to the renewable energy age has become unsupportable since this turn of events. The German government itself has stated that natural gas and other energy imports from Russia must be halted completely as soon as possible (the decision to stop coal imports was made in July 2022) – ignoring the possibility that Russia may well decide to turn off the natural gas tap of its own accord as has happened for Nord Stream 1 – and that it will probably take several years just to replace the lost Russian natural gas supplies with natural gas imports from other world markets, let alone to increase the volume of natural gas imports. These strictly quantitative considerations do not consider price relations at all. Nevertheless, more fundamental corrections to the course of the energy transition as it has been pursued in Germany for years and ambitiously stepped up by the traffic light coalition are not yet even on the agenda. In view of the acute natural gas crisis, it would be particularly obvious to revitalise domestic natural gas production, which is in decline in any case and would otherwise be completely exhausted in a few years; there are, for instance, large reserves in the deep North German shale rock that could be exploited by fracking, and production could replace imports of fracked natural gas from North America or other producers. Domestic natural gas production in 2021 amounted to a mere 50.5 bn KWh, all of 5 % of domestic consumption; 95 % of the demand had to be imported, while Germany imported more than another 60 % for (intermediate) trade and export. The Federal Institute for Geosciences and Natural Resources (BGR) estimates conventional domestic natural gas reserves at 22 bn m3, which would represent just five more years of production at the current level. In contrast, unconventional gas reserves such as coal seam gas and especially shale gas, which could be tapped by fracking, are estimated at 1,360 bn m3. (11)

The special topic of nuclear power was discussed in 2022 in the sense of a “stretch operation” of the last three German nuclear power plants, which were actually scheduled for final closure at the end of the year. The coalition parties were unable to reach any agreement, however, about longer-term lifetime extensions, much less the construction of new reactors or at least the testing of new types of reactor concepts. Not even R&D activities in this field are supposed to be continued in Germany.

If these options are definitely ruled out, however, the foreseeable longer-term natural gas shortage, the high natural gas prices that will remain in effect and the energy policy risks and problems associated with natural gas imports will leave coal as the only option for the backbone of the German energy transition, in any case for a longer period of time than previous political resolutions and declarations of intent have communicated and longer than climate activists with their more than one-sided perspective have deemed acceptable. This would moreover facilitate the foreseeably difficult structural change in the coal regions. Still, this step would require considerable modifications to the Coal Phase-Out Act, although this would give coal-fired power generation and domestic coal extraction a legal reliable basis for planning until alternatives exist that are genuinely reliable technical and economic capacities and not merely political wishful thinking. Numerous solid arguments can be put forward for suspending the coal phase-out, and they will be presented in the following. If the coal phase-out remains untouched or even moved forward, Germany would be embarking on an “energy and regional economic adventure”, as this author explained in an earlier article, and the dangers of this adventure have materialised faster than expected because of the new era. (12)

Securing electricity and heat supply with coal

The concept of the energy transition in Germany is essentially, as practiced to date, one of an electricity transition. The main building blocks are the largely completed or scheduled exits from nuclear and coal-fired power, the expansion of renewable power generation, especially from wind and PV – where progress has only partially met expectations and must be strongly accelerated in the future – and the substitution of electrification and the use of hydrogen produced using green electricity for oil and natural gas in the other sectors. If these goals are to be realised, however, total power generation must rise dramatically because electricity will be needed in future for e-mobility and for more and more electric heating equipment such as heat pumps and power-to-heat plants; moreover, enormous capacities for hydrogen electrolysis and the processes known as power-to-gas and power-to-liquids will be required, all in addition to the current uses of power that include the growing complexity of installations for modern information technologies (digitalisation). There are various scenario studies based on differing assumptions on the rise in electricity consumption and the electricity generation required to meet the demand. The study “Climate Paths 2.0” from the Boston Consulting Group (BCG) presented in October 2021, which was commissioned by and in cooperation with the Federation of German Industries (BDI), is based on a particularly broad foundation of expertise from business practice and has completely calculated a programme for a climate-neutral economy in the year 2045 (Figure 4).

Fig. 4. Power generation capacities in GW until 2030 and 2045 according to the climate pathways 2.0 study (BCG/BDI). // Bild 4. Stromerzeugungskapazitäten in GW bis 2030 und 2045 gemäß Klimapfade 2.0-Studie (BCG/BDI). Source/Quelle: BCG, BDI

This study indicates that electricity consumption in Germany in 2045 would be almost double that of 2019. The power generation capacities, i.e. the installed capacity, would have to almost treble from 225 GW to 621 GW (+276 %). Besides an increase in wind and solar power capacities (a doubling as early as 2030), an increase in natural gas-fired power capacities from 31 GW to 74 GW in 2030 (whereby coal-fired power generation would have been completely replaced as early as 2030) and to 88 GW in 2045 is assumed; another assumption is that biogas and remethanised green hydrogen would be used more and more frequently in lieu of natural gas after 2030. (13)

In short, natural gas-fired power generation would have to increase by 43 GW in addition to the more than 150 GW of new renewable generation capacity. Growth of this magnitude is equivalent to the (parallel) construction of 80 to 100 new natural gas-fired power plants, a programme of a scope that has never been seen before in such a short period of time, even in the conventional sector in Germany, and one that appears unrealistic in view of the usual planning, project and construction times – not to mention the question of whether there are enough specialist companies willing to invest the required funds and effort under the current political and economic conditions. Even if the expansion of wind power and PV, including the necessary grids, were to become possible to this exorbitant extent in the next few years, the addition of an additional 43 GW of power generation from natural gas no longer seems practically possible in view of the latest developments in the natural gas sector; supplying even existing natural gas capacities alone is likely to be a major challenge in the coming years. At the same time, the question arises as to why the coal-fired power plant capacities that in 2019 amounted to 40 GW and that are in part still available should be completely removed from the market by 2030. The proposals advanced here are to leave in place for the time being the coal-fired generation capacity of about 30 GW achieved by 2022, to reactivate as far as possible recently closed capacities, to suspend the coal phase-out for the moment and to replace the originally planned natural gas reserve for power generation with a coal/natural gas mix (Figure 4). The idea of leaving in operation one coal-fired power plant scheduled for closure for every natural gas-fired power plant that is not completed on time does not seem realistic because of the major issues in synchronising the actions and the lack of planning security. The decision to suspend the coal phase-out must be made as soon as possible to ensure adequate effectiveness and to secure the power supply for the foreseeable future.

In future, the imported natural gas (which has become scarce) should be reserved primarily for securing the heat supply and be limited at this time to power generation primarily in highly efficient combined cycle plants that simultaneously contribute to the heat supply, especially in district heating networks, via cogeneration of heat and power. This covers about two-thirds of the natural gas capacities for power generation, after all. Any further substitution of natural gas for the current generation of district heating should be halted; the same is true of any changeover to strictly open-cycle gas turbines as the supply of their energy source can no longer be guaranteed.

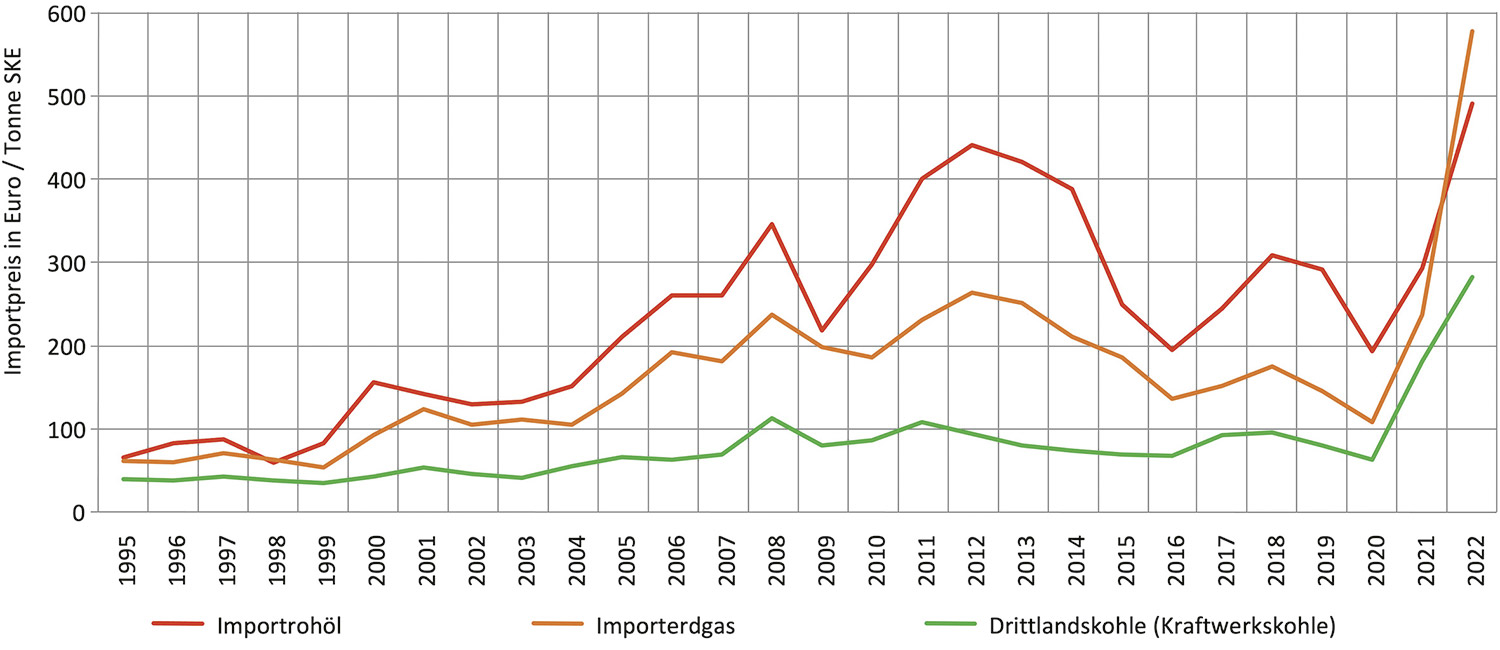

In contrast to earlier years, there are now no economic arguments in favour of a switch from coal to natural gas even if the issue of supply security is ignored. Even when CO2 costs are factored in, coal-fired electricity has for the most part had a distinct and consistent cost advantage over natural gas-fired electricity in the EU since 2021, known among experts as the “clean dark spread”. It has been known for a long time that coal, measured in terms of the import prices of energy sources without a CO2 surcharge, has always been considerably cheaper in Germany than Russian pipeline natural gas, and this trend has been on the rise since 2021; see the price development of imported hard coal compared to imported oil and imported natural gas in TCE (Figure 5). Despite the sharp rise in the price of hard coal during the same period, the price difference to expensive imported natural gas has continued to grow in 2022.

Fig. 5. Price development of selected imported energy sources. // Bild 5. Preisentwicklung ausgewählter Importenergieträger. Source/Quelle: Statistik der Kohlenwirtschaft, BAFA (bis 2018), VDKI (ab 2019), Stat. Bundesamt; Stand: Juli 2022

It is clear that the volatile and fluctuating renewable energies wind power and PV that are dependent on weather conditions need a conventional backup, a balancing and reserve capacity, because otherwise the demand cannot be covered permanently in the required scope, i.e. 24/7. This is especially true during periods in which there are strong supply disruptions or there is a simultaneous lack of wind or sunshine over a longer period of time (dark doldrums) and the electricity supply cannot otherwise be guaranteed reliably as long as there are no technologies for large, long-term electricity storage. Despite intensive R&D efforts, this is still far from the case; dark doldrums lasting more than two days occur twice a year on average and can extend to periods as long as two weeks, and periods of low wind and solar power are a constant factor (every night for PV). The pumped-storage power plant capacities available in Germany are far too small for this purpose, and for the foreseeable future, the number and costs of electric batteries will prevent them from offering solutions for more than so-called balancing power and reserves in a range of minutes. (14) Hydrogen could be the solution to the long-term storage problem, but it is not yet an electricity storage system itself; it can serve solely as a storable raw material for remethanisation, a process that in turn means additional electricity demand and low energy efficiency. Although high energy policy hopes are being placed in the hydrogen route because of its theoretically considerable storage potential and its close link to natural gas technology, capacities are still only low. This is another area requiring large-scale expansion, but apart from other practical obstacles and now the natural gas issue, it will remain blocked for the time being by the lack of economic viability and the need for enormous subsidies. (15) This finding currently applies to the relatively densely populated and highly industrialised Germany as well as internationally, which is why the state of affairs can be summed up as follows in agreement with Vaclav Smil: “And even in this era of high-electronic miracles, it is still impossible to store electricity affordably in quantities sufficient to meet the demand of a medium-sized city (500,000 people) for only a week or to supply a megacity (more than 10 M people) for just a half day.” (16)

Existing coal-fired power plants can do very well what natural gas can no longer do and hydrogen will not be able to do for a long time to come. Modern coal-fired power plant technology offers a flexible mode of operation similar to that of natural gas-fired power plants. This was the conclusion reached by the green think tank Agora Energiewende as early as 2017 on the basis of a study by Prognos and Fichtner. The study notes that “electricity systems that have so far been based primarily on coal-fired power plants offer much more room for the expansion of renewable energies than is often claimed.” The conclusion is that coal-fired power plants “are not necessarily an obstacle to the expansion of renewable energies.” As examples from Germany and Denmark demonstrate, even old coal-fired power plants can be operated “almost as flexibly as natural gas-fired power plants” with little conversion and relatively little economic effort, and by regularly ramping up and down according to demand, they can “adapt their electricity production far more flexibly to the fluctuating output of wind and solar power plants than has often been assumed up to now.” This makes it possible to make this coal-fired electricity “more climate-friendly at low cost while maintaining security of electricity supply.” (17) This does not even consider that coal can also be burned in combination with biomass or waste, which provides additional flexibility in fuel input.

This statement must be seen against the background that coal continues to be a reliable and cheap source of energy for electricity generation and contributes no less than 37 % to power generation worldwide and globally continues to be the Number One energy source for electricity generation. Germany’s share of coal-fired power currently corresponds almost exactly to the global average. But it could show precisely how this contribution can be reconciled with the energy transition. At the same time, Germany can continue to cover its demand for lignite completely from domestic deposits, insofar and as long as domestic lignite production is maintained. Although there are still substantial hard coal deposits, they have no longer been accessible since the complete shutdown of the domestic hard coal mining industry and, from a strictly technical point of view, could be opened up again only in the very long term at best and in isolated cases. What is available, however, is a stable, relatively diversified and logistically well-developed supply from the world coal markets that excludes procurements from Russia; Germany has been importing from these markets – whether from Poland, South Africa, Colombia, the USA to Australia and others – for a long time. Virtually nothing has ever been imported to Europe and Germany from Indonesia, the world’s largest export country for steam coal, mainly because of its low grade, but this issue appears to be surmountable technically and economically. The Indonesian coal industry is now in negotiations with several Western countries. (18)

If the recommendation in this article is for the indefinite use of coal or a coal/natural gas mix in electricity generation, it should by no means be understood as an objection to the expansion of renewable energies, but rather for use as the backup to these sources. When (perhaps one day in the not-too-distant future) sufficient regenerative capacities and long-term storage facilities based on hydrogen – or whatever alternatives energy technology research may yet develop – have been built, the coal- and natural gas-fired power plants can finally be taken offline without any worries about the security of electricity supply – but only then. The operational start-up of the new energy supply must precede the shutdown of the previous supply, not vice-versa.

Since, at the same time, the course set by the energy transition on the electricity market is no longer about genuine competition, but only about the future backup function outlined above prioritising renewables, there is a lot to be said for establishing a so-called capacity market or comparable capacity mechanisms for coal and natural gas power in the future. A capacity market designates an electricity market on which the actual production or consumption of electricity quantities is no longer traded and remunerated – the so-called energy-only market – but rather solely the services provided to maintain balancing and reserve capacities and their controllably secured use. The establishment of this type of market has been the subject of dispute in Germany for years. Other European countries such as France or the UK have established capacity markets, which shows that EU-compliant solutions are possible. A reform of the electricity market is already on the agenda in Germany. The German Electricity and Water Industry Association (BDEW), which had previously discussed the issues comprehensively, diligently compiled once more in 2021 the aspects that must be considered from the perspective of the security of the electricity supply in general, albeit still based on the premise of natural gas as a bridge to the electricity market of the future (19). This premise has now fallen by the wayside, but the imperative to secure the electricity supply remains unchanged.

Hardly any disadvantages for climate protection from coal backup

While there are usually no serious objections to the argument that coal provides security of supply and is cheap, the usual criticism is that coal is the energy source that is most harmful to the climate and must therefore be the first to be ousted from the energy mix for the realisation of climate policy goals. Apart from the fact that this approach of a complete exit is difficult to reconcile with the basic principle of a balanced energy mix and that the initially chosen alternative of natural gas is no longer viable in view of the geopolitical situation and developments, the disadvantages of a coal backup instead of a natural gas backup in power generation are also much smaller from a climate protection viewpoint than they appear in the often truncated political debates.

First of all, it should be pointed out that the climate debate in Germany is characterised by gross disproportionality, especially in the contributions of many media and climate activists. Every policy, including climate policy, must take into account a multitude of interactions, side effects and consequences and conflicting goals must be balanced. That is why energy policy has always pursued a balanced triangle of goals of environmental compatibility (which is more than climate protection), security and economic efficiency of the energy supply. Likewise, every policy committed to sustainability, including energy and climate policy, must carefully weigh ecological aspects with economic and social aspects.

Moreover, climate protection is a global issue that can ultimately be solved solely on a global scale and not even remotely by the climate policy in Germany alone, no matter how ambitious it may be. Germany’s share of global energy-related CO2 emissions, which according to energy data from the Federal Ministry for Economic Affairs and Climate Protection (BMWK) totalled 34,040 Mt in 2019, was exactly 2 %. More than half of CO2 emissions worldwide (50.5 %) comes from Asia/Oceania; China alone accounts for almost 29 % of global CO2 emissions. This represents about twice the share of emissions of the USA (14.7 %) and more than three times that of the entire EU and the UK (8.6 %). Even if Germany, with its current share of only one-fiftieth, could suddenly achieve climate neutrality and immediately reduce all emissions to net zero, not only would this have no impact on 98 % of global CO2 emissions; the decrease would also be completely wiped out by the increase in emissions in the rest of the world within just 15 months (based on the average annual rate since 1990 of approximately 1.6 %). Of course, Germany could play a certain role as a role model and pacemaker in climate policy. But this has obviously not made any impression on a global scale, which is what matters here. The model of the German energy transition, including the coal phase-out, is not being imitated in most of the world, and even neighbouring European countries pay little attention to it; they are taking very different tacks in their energy policies and not only, as is quite obviously the case, in their nuclear energy policies.

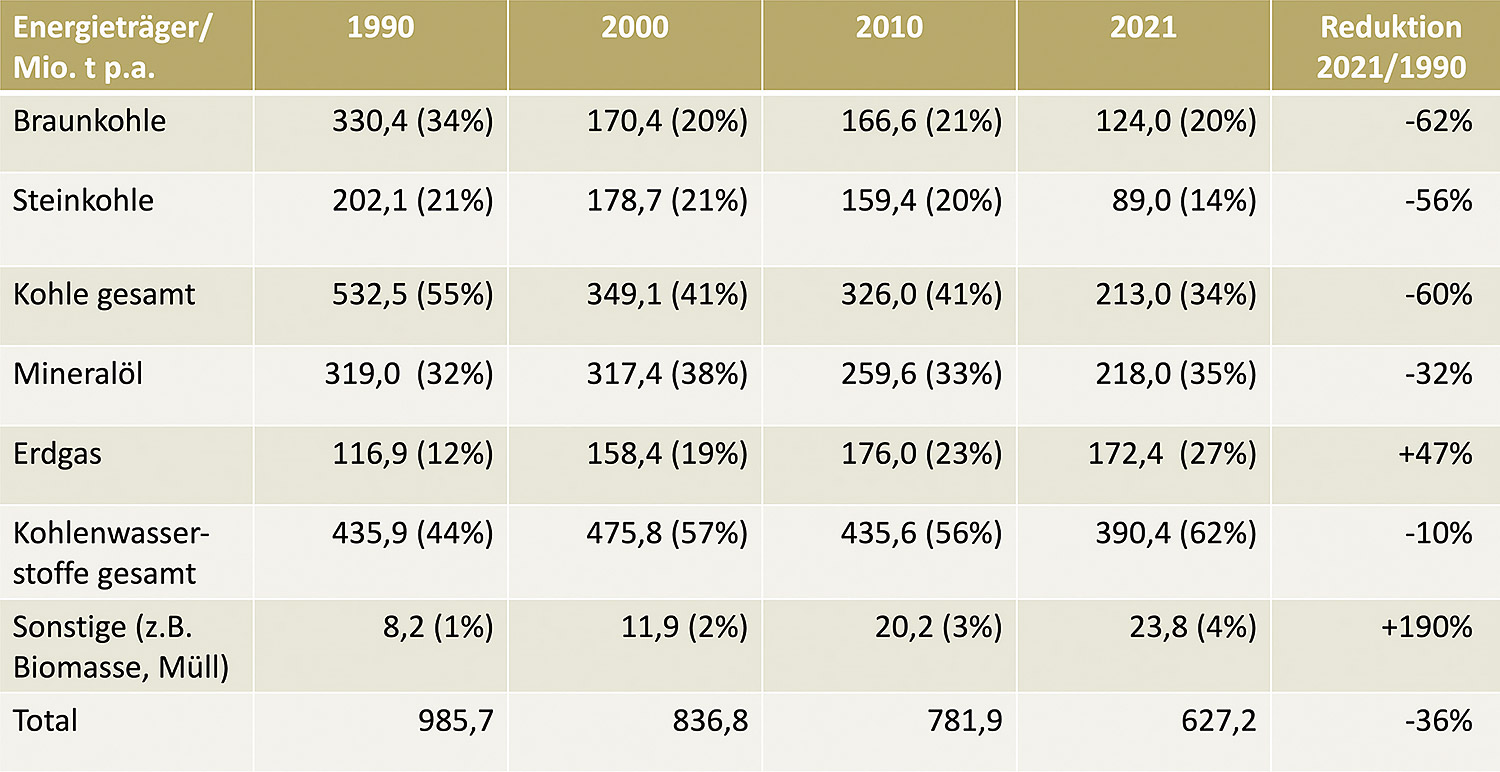

The contribution of coal-fired power generation in Germany to global CO2 emissions is about 0.6 %, so the coal phase-out in this country would fizzle out on a global scale in a few months. The importance of the coal phase-out is often overblown, however, even from a strictly national perspective. The great breakthrough toward national climate neutrality cannot be achieved with the exit from coal-fired power generation and other coal use alone. The share of energy-related CO2 emissions in Germany produced by coal is simply too low in comparison with the hydrocarbons oil and natural gas. To be sure, lignite was still the energy source with the highest CO2 emissions in Germany in 1990 and coal as a whole (lignite and hard coal combined) accounted for more than half. But these ratios have changed fundamentally in the last three decades. In 2000, oil was the energy source with the largest share of domestic CO2 emissions, and most recently (2021) oil alone accounted for 35 % of emissions, more than coal as a whole (34 %). Although there was a major reduction of 32 % in CO2 emissions from oil consumption between 1990 and 2021, the reductions in hard coal (– 56 %) and lignite (– 62 %) were much greater. In contrast, natural gas was the only conventional energy source to record a considerable increase of 47 % – being used partly as a substitute for oil, partly as a substitute for coal. In the meantime, all coal now accounts for only 34 % of energy-related CO2 emissions in Germany, but hydrocarbons as a group account for 62 % (Figure 6).

Fig. 6. Development of CO2 emissions in Germany in comparison with other energy sources. // Bild 6. Entwicklung der CO2-Emissionen in Deutschland im Energieträgervergleich. Source/Quelle: BMWK Energiedaten 2022 (hier Daten bis 2010); Schiffer in ET 3/2022 (Daten für 2021); eig. Berechnungen

In other words, a complete coal phase-out can take the country at most one-third of the way to national climate neutrality; an increase in the use of natural gas would lower this figure even further. It must be clear to every decision-maker, every company and every citizen that the goal of climate neutrality cannot be achieved simply by phasing out coal. Quite the contrary – exit plans for natural gas and oil with their broader and more diffusely distributed direct consumers are also required, and that means that there is a lot more hard work ahead when it comes to climate policy – and tackling these tasks began later in Germany. The communication in the media on this topic is still woefully inadequate.

From a climate policy standpoint, prioritising the coal phase-out cannot in any case be justified by the bare facts. Conversely, in terms of climate protection, continuing to use coal for power generation for the time being does not de facto present any significant disadvantages compared to natural gas as a “bridge” because – excluding pipeline transports from Russia and in consideration of declining deliveries from other European countries – a global standpoint that includes the supply routes reveals that liquefied gas transports of US shale gas have a worse CO2 balance than domestic lignite and imported hard coal; liquefied gas transports by ship from Algeria or Qatar are only slightly better. (20) This does not even address the issue of methane leaks during natural gas production or leaks during transport or conversion processes.

Determining climate policy must also recognise that the issue here is solely about an increasingly limited role for coal on the electricity market as a balancing and reserve capacity for renewables and not about increasing the share of current coal-fired electricity generation itself. As the professional website “Tech for Future”, which also assumes the collapse of the natural gas bridge (“Natural gas as a bridge technology is dead”), has shown, the significant factor for CO2 emissions from power generation is not how much coal capacity is shut down, but how much coal is actually combusted in the power plants. Coal-fired power plants that operate for merely a few hours to generate electricity when there is not enough wind and solar power available, but are otherwise only in standby mode as a safety reserve, also have correspondingly low CO2 emissions. Tech for Future has calculated a case for the lifetime of a coal-based backup for 2030, assuming that annual electricity consumption in Germany will increase to 700 TWh, 30 GW of natural gas-fired capacity will be added and the expansion target for renewable electricity of 80 % will be achieved. The weather data from 2015 to 2021 are assumed to be representative. In this case, a balancing and reserve capacity of 40 GW based on coal (50 % each for lignite and hard coal) would have an average utilisation of only 3.6 % or 319 h/a. Although the 5 GW most used for backup power would reach as much as 70 % capacity utilisation, other coal-fired power plants would hardly operate at all, and the 5 GW least used for backup power would post a mere 0.05 % capacity utilisation or 4 h/a, and over the long run, they would be completely idle in some years. In total, only 1.6 TWh of coal-fired electricity would be produced in 2030 instead of the 163 TWh of 2021. That would be a decline of 99 %, and the same would be true of the CO2 emissions from the remaining coal-fired power generation – without a complete coal phase-out, but with security of supply through reserve coal-fired power. (21)

The reputable consulting firm McKinsey also assumes that a premature coal phase-out can no longer be achieved under any circumstances on the energy transition journey in view of the natural gas shortages, even if natural gas continues to make an important, but smaller contribution. As part of the McKinsey Energy Transition Index, three electricity mix scenarios incorporating a large number of energy industry assumptions and variants were calculated for 2030, and, in consideration of the continuing scarcity and higher prices of natural gas, all predict that the share of coal-fired power will remain substantial and that its role will go beyond that of a mere security reserve. The “Federal Government Plan” scenario presumes that renewable electricity production, electrification and hydrogen capacities will be expanded as planned and remains committed to the statutory coal phase-out by 2038. Nevertheless, coal-fired power generation would have to contribute 63 TWh in 2030 “to ensure seamless supply.” This would represent a reduction of 61 % compared to 2021 and an equivalent decline in the resulting CO2 emissions – a total decrease of 84 % from coal-fired power generation since 1990. The planned emission reduction target in the electricity sector would nevertheless still be achieved. Significantly more coal-fired power generation would be expected in Germany in 2030 in the two alternative scenarios “Largely self-sufficient” and “Electricity from Europe” owing to price effects. In these scenarios, it is presumed that Germany will accelerate the expansion of renewable energies, but that it will not fully achieve its ambitious targets by 2030 and will import even less natural gas. This would also drive the CO2 emissions of the power sector to a relatively high level. According to McKinsey, the so-called secured reserve margin, i. e. the share of necessary secured output, is even now “on the brink”. If coal were to be phased out by 2030, this would fall into negative territory, i.e. the security of the power supply could no longer be guaranteed at all times in the future. (23)

The utilisation of CCS or CCUS technologies (capture and storage and/or utilisation of CO2) is an option that could eliminate the remaining CO2 emissions from coal-fired power generation in the long term and largely resolve the conflict between the security of supply advantage and the climate protection disadvantage of coal-fired power generation. Such technologies are available and should be used in any case for the unavoidable residual emissions in certain other sectors of the economy. But future coal-fired power generation would concern solely residual emissions as well. There would also be a number of opportunities for the economic use of these emissions such as the production of special plastics or synthetic fuels or the addition of carbon required during the remethanisation of hydrogen. (22) The Ethics Commission “Secure Energy Supply” even recommended a German “clean coal” programme of this type involving the development of commercial cycles for the use of CO2 in 2011 to as part of the nuclear power exit. (24) This recommendation is now current again.

Consider the raw material aspects of a coal phase-out more comprehensively

The legally required review of the coal phase-out in Germany also requires, as mentioned above, the consideration of raw material aspects, explicitly referring to gypsum for the construction industry. Gypsum that can be used as a building material has always been produced in relatively large quantities during the flue gas desulphurisation of coal-fired power plants. In future, increasing quantities of this product would have to come from mining the limited natural gypsum deposits in this country or from imports. The supply prospects of other by-products of coal-fired power plants such as fly ash or boiler sand, which are also in demand as aggregates in the construction industry, should also be considered. Additionally, raw coal plays a special energetic and material role in the cement and lime industries. So the coal phase-out has quite a significant impact on the construction sector. Suspending the coal phase-out would ease the supply situation for this industry, which is also essential for the achievement of many other goals and projects during the energy transition, and alleviate the time pressure for its adaptation. These and other side and consequential effects must always be taken into account.

The German coal phase-out has been conceived as a phase-out of coal-fired power generation, the main user of lignite and hard coal. It does not concern directly the material uses of coal, from its niche functions on the heating market as briquettes for heating to the use of coking coal and coke for the production of crude steel or in the foundry industry to the many diverse uses in the chemical industry. These sectors are affected by various other climate policy measures that are tantamount to a coal phase-out without any explicit deadlines. A slower withdrawal from the coal market could make sense and be helpful in managing the transformation for these areas of material coal use, especially since the status of natural gas as a bridge has become questionable here as well.

One example can be seen in the lignite-based montan waxes produced by Romonta GmbH from Amsdorf in Saxony-Anhalt, which has been active in lignite refinement for 100 years; it operates its own opencast pit and is the world’s largest producer of raw montan wax, a “hidden champion”. Romonta’s products are used in a multitude of applications from construction to the capital goods and consumer goods industries. (25) This example is intended merely to demonstrate that the raw material aspects associated with the coal phase-out and their economic interrelationships should be the subject of more comprehensive consideration than is seen in the general demand for the fastest possible end to the use of coal.

Likewise, sufficient clarification of the raw material basis for renewable energies or hydrogen technology that are seen as alternatives and of the necessity to secure supply even in the face of growing global demand and the concentration of raw material deposits in critical supplier countries must be explicitly demanded to prevent a predicament in these areas similar to the one currently being experienced in obtaining supplies of natural gas. The energy transition requires enormous material resources; in addition to the classic construction raw materials mentioned above, large quantities of special raw materials, especially “critical” metals, will be needed. Some of these materials are even now in short supply, others are controlled by the near-monopolies of single countries such as China, which is why experts in this field warn of the next dependencies as recently described by the Spektrum der Wissenschaft. Although there are possible solutions to this problem such as a return to the mining of domestic deposits and more research in post-mining, they are not necessarily politically or socially popular and will take a long time. (26)

More time and maturity for regional structural change

A suspension of the coal phase-out would also have clear regional policy benefits. The energy crisis triggered by the new era is proving to be accompanied by the risk of a recession and grave macroeconomic disruptions. This kind of problematic macroeconomic situation arising from an external shock also makes the regional structural change in particular more difficult; if possible, the transformation should (in the sense of Schumpeter’s “creative destruction”) lead to new value creation and generate jobs to replace the previous production methods that are disappearing at existing locations, but may not have such a creative impact when faced with adversity. This is especially true for the coal regions, which are deprived of their industrial core by a politically driven coal phase-out. (27)

Under such conditions, a successful regional structural change in the course of the coal phase-out must be given more time and the accompanying greater opportunity to mature rather than being confronted with an even shorter time span. Decades of experience with structural change in the Ruhr Valley consequent to the decline of the coal and steel industries prove – as “lessons learned”, so to speak – that it takes 15 to 30 years to restore previous industrial sites to marketability and to turn them into regional economic assets. There are neither any general nor coal-specific patent remedies for structural policy, only the realistic realisation that customised solutions and stamina are needed for each of the locations and regions so that there is time to overcome misjudgements, resistance and setbacks. (28) A coal phase-out by 2038 would be at the earliest possible boundary of the range based on experience; even 2045 would be no better than in the intermediate range, while 2030 would clearly be too early.

The latter premise is also supported by initial findings regarding the structural change in the East German lignite regions that has been politically initiated. It has got off to a rather sluggish start and, according to an analysis by the Cologne Institute for Economic Research (IW), is proceeding “far too slowly” for achievement of an exit before 2038; the analysis concludes: “It is still not possible without coal.” At another point, it notes: “The war in Ukraine also demands a rethink,” because it has already made some of the assumptions of the structural support launched in 2020 obsolete. Even without the factor of the new era, however, the originally assumed speed of planning and approval procedures has been too slow in practice, and other planned measures have not been adequately focused. (29) One example worth mentioning is the ICE railway line from Berlin via Cottbus to Görlitz, planned as a major infrastructure project for the Lusatian mining area; progress has been minimal because fundamental planning decisions are still lacking. Nor is the envisioned expansion of broadband networks and 5G mobile communications making much headway, not only in the lignite regions, but here as well. Planning for the project to locate the Federal Highway Authority in Leipzig has progressed a little further. And yet, the IW plausibly asks, “What is the benefit of jobs in a booming major city if lignite jobs are lost in rural regions (of the Central German coalfield)” and, moreover, if no one considers that the typical “requirements for government jobs differ greatly from the requirements of industrial jobs that are being lost?” The focus must be instead on attracting new, private companies, above all from industry, to the regions. In general, the IW notes that “Success in the structural change requires – in addition to the right measures – above all time.” (30)

Government infrastructure measures such as those included in the Act for the Structural Strengthening of Coal Regions in particular appear to be an essential, but by no means offer an adequate single condition for successful regional structural change. They create the prerequisites for private economic activities. In the German coal regions, the initial objective is in part the clearing of backlogs that will enable these areas to come close at least to catching up with structurally stronger regions. The decisive factor, however, is the sparking of new private sector activity that will generate growth and employment. The IW previously investigated ways and means of encouraging private investors to become active in the coal regions by establishing government framework conditions. Similarly, there is a whole range of so-called place-based job policies that could be used or reviewed as possible supplements, from financial incentives such as specific grants and tax breaks to public material services provided locally such as tailored counselling and qualification offers. (31) However, the work is not done with the development of these actions; they must also be constantly readjusted and allowed to mature in the competition among locations to become effective.

There is more to this approach than merely attracting and locating companies that previously operated elsewhere to the coal regions or founding new businesses and start-ups in these regions; adequate support must be provided in this sense as well, of course, but it is difficult to predict either the scope or timeline of the success of these actions. Support is also needed for the existing regional economy at the locations that will be especially impacted, whether directly or indirectly, by the coal phase-out, including first and foremost the energy suppliers that generate electricity using coal and the coal mining companies themselves. They must be given sufficient leeway and opportunities to contribute their innovative potential to regional structural change and, as far as possible, to preserve their know-how and their established value chains through new uses (repurposing). (32) Essential prerequisites for this are that the stability of the existing core business is maintained long enough and that the new activities have profitable useful lives sufficient to finance the necessary investments for the conversion and reorientation of the sites. Another factor in addition to the strictly economic criteria is a time dimension, namely, the transition time, which encompasses all the necessary planning and approval phases and the time required for securing and cleaning up the old sites, procuring materials, building or converting the physical capital and infrastructure, developing all the necessary supply sources (including all the measures necessary for recruiting and/or qualifying personnel) and finally, for operational startup, market development and establishment of the new productions. The shorter the available transition period, the greater the economic risks and the smaller the opportunities for regionally sustainable change tend to be.

The German coal industry itself has long been actively involved in the conversion of coal regions in the direction of the new climate-friendly energy world that is planned. The domestic lignite industry, e. g., is massively expanding renewable energies in combination with battery and/or hydrogen projects in its post-mining areas in all coalfields. The assumption, however, is that “green power remains coupled with secured power” and that structural development is based on reliable specifications. A coal phase-out by 2030 would therefore be “difficult to imagine” for them; even the legal exit date of 2038 with the assumption of a natural gas bridge for the energy transition “poses major genuine challenges for the coalfields” (Figure 7). (33)

Fig. 7. Previous closure plan for lignite plants from the regional perspective. // Bild 7. Bisheriger Stilllegungsplan Braunkohlenblöcke in regionaler Perspektive. Source/Quelle: BMWi

Just how critical the time factor is for the entire public regional planning concerning the coalfields and how fatal too rapid a coal phase-out or too great the transformation pressure can be for regional income and employment development is something that the eastern German states in particular experienced in the 1990s. And the example of the West German coalfields in the Ruhr and Saar regions with their persistently above-average unemployment and poverty rates after a decades-long adjustment process leading up to the final exit gives little reason to hope that structural change can be successfully managed in a few years.

This is not contradicted by the fact that the massive structural support provided to coal-mining regions under the Act for the Structural Strengthening of Coal Regions can, if successful, trigger a positive structural change and leave the coal-mining regions in a better economic position than before. This is only possible, however, if the funds pledged until 2038 really flow on time and generate the best possible results. This is at least the conclusion of the study carried out by IW Consult on behalf of the state government of North Rhine-Westphalia on the specific job and added-value effects of the structural support in the Rhenish mining area provided in the Act for the Structural Strengthening of Coal Regions that was completed and submitted at the end of 2021. (34) It determined that in the trend scenario it would be possible to leverage the structural funding of 14.8 bn € committed by the federal and state governments in 2020 (in conjunction with private investments) to a value creation potential of around 53 bn € by 2038. This would create 27,000 new jobs in the region and beyond, which would arithmetically more than compensate for the 14,400 jobs lost through the exit from lignite-based power generation. Of course, these predictions are still far from becoming reality; they are merely scenario calculations for economic potential that is dependent on many preconditions, including the special structural conditions of the Rhenish mining area, which are more favourable than those of the eastern German lignite regions. Another key prerequisite is the planned coal phase-out by 2038. A coal phase-out advanced to 2030 would – as this study explicitly points out – mean several thousand fewer jobs and several billion euros in lower added value, all other things being equal. The natural gas crisis and the new era, however, have invalidated the initial assumptions. The study also explicitly refers to strong economic interactions with other sectors that go beyond the coal industry’s direct upstream and supplier sectors. This is particularly true of energy-intensive industries such as aluminium that provide about 50,000 jobs in and around the region and for which lignite has been a cost-effective and reliable energy supplier; their future is critically dependent on their products and production processes remaining competitive when energy costs are taken into account. IW Consult refers to calculations by the economic research institute RWI indicating that sharply rising energy prices would jeopardise as many as 20,000 jobs in these industries in the Rhenish coalfield alone and worsen the regional employment balance overall. (35) This is exactly what happened in 2022.

There is also a “pessimistic scenario” for the planned coal phase-out by 2038, in which value creation and employment are considerably lower than in the trend scenario. And this could result from “the lack of the desired success in integrating companies, more extensive deadweight and substitution effects (in the purchase of machinery and equipment, for instance), failure to realise synergy effects among projects and the related reduced significance of the development of spillover effects.” In any case, it is assumed that the key factor “selection and prioritisation of projects” is implemented as well as possible in economic terms, that objectively reasonable evaluations and recalibrations of projects are carried out regularly, that bureaucratic obstacles and pitfalls are avoided or, e. g., that existing land availability can be used strategically and optimally and that industrial land area potential can be sufficiently realised. (36) These are, so to speak, inherent risks to the success of any structural support, even when general conditions are stable, that are realistically virtually unavoidable and occasionally require time-consuming correction processes during the practical realisation. This alone speaks in favour of revising the deadline in 2038 to a later time or as a minimum of relaxing the strictness of compliance with this date.

However, if negative macroeconomic developments such as the current crisis even today reduce the impact of initial investments (transport infrastructure, research and education, digital transformation, etc.) that provide the decisive stimulus and promise so-called quick wins, especially in the first years of structural support, and consequently, e. g.,less private capital can be leveraged for the time being or public contracts cannot be performed as planned, the resulting direct, indirect and induced effects and the associated spillover effects will be reduced or at least delayed and the expected overall effect on regional economic growth and employment will be diminished. This also has a qualitative impact on the content-related objectives of the structural programme briefly described in the study that is intended to make the Rhenish mining area a “model region” both for green energy with a secure supply and modern competitive industry and for sustainable resource use and agrobusiness. (37) The new era in energy policy has also changed the preconditions for these projects even more than significantly and throttled the pace.

Fig. 8. Coal power – the resilient bridge for the energy transition. // Bild 8. Kohlestrom – die belastbare Brücke für die Energiewende. Photo/Foto: STEAG

The impact on all other coal regions and locations in Germany, whether based on lignite or hard coal, is similar (Figure 8). Suspending the coal phase-out while continuing the initiated structural support could also mitigate these negative effects in regional policy and improve the prospects for successful structural change in the long term. It is not only in the interest of the future of the coal regions to do what is now indicated in the energy policy without neglecting what remains necessary in the regional policy.

References / Quellenverzeichnis

References / Quellenverzeichnis

(1) Siehe die Darstellung zu Kohleausstieg und Strukturwandel des Bundesministeriums für Wirtschaft und Energie, seit Ende 2021 für Wirtschaft und Klimaschutz (BMWK) unter https://www.bmwk.de/Redaktion/DE/Artikel/Wirtschaft/kohleausstieg-und-strukturwandel.html

(2) Koalitionsvertrag „Mehr Fortschritt wagen. Bündnis für Freiheit, Gerechtigkeit und Nachhaltigkeit“ zwischen SPD, Bündnis 90/Die Grünen und FDP vom 28.11.2021, hier S. 58f.

(3) Siehe WELT vom 15.8.2022: Ampel verschiebt wohl ersten Bericht zum Kohleausstieg. Energiewirtschaftliche Tagesfragen 72 Jg. 2022, H. 5, S. 35 – 40.

(4) Vgl. Umbach, F.: Erdgas als Waffe. Der Kreml, Europa und die Energiefrage. Berlin 2022, S. 51f. sowie die Rezension zu diesem Buchessay von K. van de Loo: Erdgas als Waffe – wider die geopolitischen Illusionen bei der Energie- und Rohstoffversorgung. In: Energiewirtschaftliche Tagesfragen 73. Jg. (2022) H. 9, S. 59.

(5) Siehe Umbach 2022, S. 46ff, 53ff.

(6) Vgl. ebenda S. 7ff.

(7) Siehe ebenda S. 71ff.

(8) Handelsblatt vom 29.8.2022: Energiekrise: Wirtschaftsminister will Strompreisreform.

(9) Siehe zum Ersatzkraftwerke-Bereithaltungsgesetz, wichtigen Details und Begründungen: https://www.bundesregierung.de/breg-de/themen/klimaschutz/gasersatz-reserve-2048304

(10) Handelsblatt vom 25.8.2022: Industrie in der Energiepreisfalle.

(11) Siehe BGR Energiestudie 2021- Daten und Entwicklungen der deutschen und globalen Energieversorgung, insb. S. 17ff., abrufbar unter: https://www.bgr.bund.de/DE/Themen/Energie/Downloads/energiestudie_2021.html

(12) van de Loo, K.: Der Kohleausstieg – ein energie- und regionalwirtschaftliches Abenteuer. In: Mining Report Glückauf 155 (2019) H. 2, S. 178 – 193.

(13) Siehe BCG-Gutachten (i. A. BDI): Klimapfade 2.0. Ein Wirtschaftsprogramm für Klima und Zukunft. Berlin 2021, hier insb. S. 11.

(14) Siehe Niederhausen, H. (Hrsg.): Generationenprojekt Energie-wende. Elektroenergiepolitik im Spannungsfeld on Vision und Mission. Norderstedt 2022, insb. S. 35ff., 127ff., 237ff.

(15) Vgl. ebenda insb. S. 109ff., 251ff.

(16) Smil, V.: How the world really works. A Scientist’s guide to our Past, Present and Future. Dublin 2022, p 33.

(17) Siehe zu den Schlussfolgerungen von Agora Energiewende aus den Studienresultaten: https://www.agoraenergiewende.de/fileadmin/Projekte/2017/Flexibility_in_thermal_plants/PM_Agora_FlexCoal_06062017.pdf, ferner die Studie von Prognos und Fichtner selbst „Flexibility in thermal power plants. With a focus in existing coal-fired plants“, abrufbar unter: https://static.agora-energiewende.de/fileadmin/Projekte/2017/Flexibility_in_thermal_plants/115_flexibility-report-WEB.pdf

(18) Zu den Steinkohlenimporten nach Deutschland und der Kohle-weltmarktsituation siehe den Jahresbericht des VDKi – Fakten und Trends 2021/22. Berlin 2022.

(19) Siehe BDEW: Fakten und Argumente – Versorgungssicherheit Strom. Berlin 2021, abrufbar unter: https://www.bdew.de/media/documents/20210930_Awh_BDEW-Fakten-und-Argumente_Versorgungssicherheit-Strom.pdf

(20) Siehe Niederhausen, a.a.O., S. 302ff.

(21) Die Berechnungen von Tech for Future sind dargelegt und abrufbar unter: https://www.tech-for-future.de/kohleausstieg/

(22) Siehe Niederhausen, a.a.O., S. 63ff., 326f.

(23) Siehe Energiewende-Index | Germany | McKinsey & Company sowie dazu den einschlägigen Fachartikel von Vahlenkamp, T. et al.: Strommix 2030: Kann Deutschland von Energieimporten unabhängiger und gleichzeitig klimaneutral werden? In: Energiewirtschaftliche Tagesfragen 72. Jg. (2022) H. 9, S. 53ff.

(24) Abschlussbericht der (nur temporär eingesetzten) Ethik-Kommission „Sichere Energieversorgung“ vom 30.5.2011: Deutschlands Energiewende – ein Gemeinschaftswerk für die Zukunft steht zum Download zur Verfügung u.a. beim Nachhaltigkeitsrat: https://www.nachhaltigkeitsrat.de/wp-content/uploads/migration/documents/2011-05-30-abschlussbericht-ethikkommission_property_publicationFile.pdf

(25) Eine Selbstdarstellung der Romonta und ihrer Produkte findet sich unter: https://www.romonta.de/de/unternehmen

(26) Siehe dazu etwa den warnenden Artikel im Spektrum der Wissenschaft vom 3.4.2022: Die Energiewende bekommt ein Rohstoffproblem. Abrufbar unter: https://www.spektrum.de/news/fuer-die-energiewende-werden-die-rohstoffe-knapp/2005387. In der Nachbergbauforschung wird u. a. eruiert, wichtige Wertstoffe für die Energiewende aus Grubenwässern stillgelegter Bergwerke zu gewinnen, siehe beispielhaft das Projekt IAW33 des Forschungszentrums Nachbergbau an der TH Georg Agricola in Bochum; mehr dazu unter: https://fzn.thga.de/wertstoffe-aus-grubenwasser/

(27) Vgl. dazu etwa van de Loo, K.: Energie- und regionalökonomische Konsequenzen der Kohlekommission. In: Energiewirtschaftliche Tagesfragen 69. Jg. (2018) H. 10, S. 12ff.

(28) van de Loo, K.; Brüggemann, J.: Nachbergbauforschung zu Reaktivierung und Transition. In: Mining Report Glückauf 157 (2021) Nr. 2, S. 127 – 139, hier insb. S. 137.

(29) Die betreffende Analyse des IW vom 1.9.2022 ist abrufbar unter: https://www.iwkoeln.de/presse/iw-nachrichten/klaus-heiner-roehl-noch-gehts-nicht-ohne-kohle.html

(30) Ebenda.

(31) van de Loo, K.; Tiganj, J.: Beschäftigungsimpulse für (Kohle-) Nachbergbauregionen. In: Mining Report Glückauf 157 (2021) Nr. 1, S. 22 – 39.

(32) Vgl. ebenda S. 37.

(33) Siehe dazu das Interview mit dem DEBRIV-Vorsitzenden Philipp Nellessen unter dem Titel „Energiekrise, Strukturentwicklung und Versorgungssicherheit“. In: Energiewirtschaftliche Tagesfragen 72. Jg. (2022) H. 9, S. 19 – 22.

(34) Diese Studie von IW Consult im Auftrag der Landesregierung NRW ist abrufbar unter: https://www.wirtschaft.nrw/pressemitteilung/arbeitsplatz-und-wertschoepfungseffekte-rheinisches-revier

(35) Ebenda S. 14.

(36) Ebenda S. 50ff.

(37) Vgl. ebenda S.15.