The manufacturers of machines for extraction and preparation of raw materials have also been shaken by the coronavirus pandemic. The figures underline this. In reaction to this, the sector is working hard to reinvent itself. Everyone agrees here that driving forward new developments and digitisation of processes are the best ways out of the crisis.

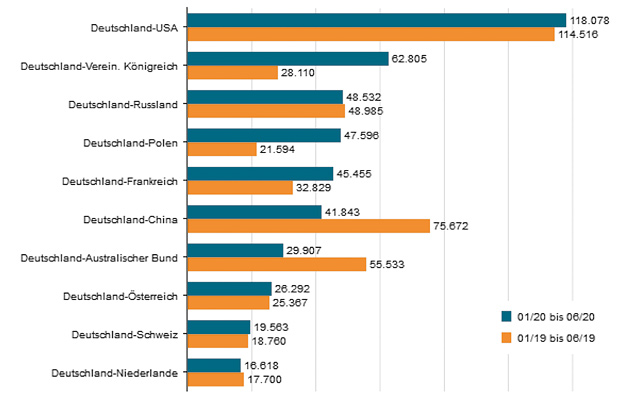

Fig. 1. Exports of German mining suppliers – comparison of first half 2020 with first half 2019. Source: VDMA

The 145 manufacturers of mining machinery in the VDMA Mining Association, based in Frankfurt/M./Germany, began 2020 with weak revenue figures as a result of the sharp decline in incoming orders at the end of 2019. The number of new orders has also remained at a low level this year, both in the first quarter (– 54 %) and in the second quarter (– 32 %). For the first half of 2020, this represents a total drop in incoming orders of 43 % (Figure 1).

In terms of revenue development, companies were initially still able to benefit from the good level of orders received in the first half of the previous year. However, the pronounced collapse of 51 % in the first quarter can also be attributed to a statistical base effect resulting from the 2018/2019 boom. Sales revenue in the second quarter of 2020 was even 17 % above the same period of the previous year – with customers throughout the world continuing to place plenty of orders well into the summer of 2019. Ultimately, however, sales revenue in the first half of the year was 21 % below the same figure from the previous year.

Global exports displayed a similar trend. In the first half of the year, they remained 11 % below the previous year’s figure, reaching a value of 760.2 M €.

While exports to the US continued to increase and Russia maintained its level, exports to China declined sharply from 75.6 to 41.8 M €. This left China, for a long time the industry’s most important single market, lagging behind in 6th place. The importance of the eurozone is really showing itself here. Among other things, the strong exports to Great Britain can be attributed to a major railway project, for which “Made in Germany” tunnel boring machines are being used.

The coronavirus pandemic has only played a minor part in the drop in exports to China. The nationalistic tones and the objective of the Chinese Communist Party to develop the country into a leading technical nation are having an ever greater impact on the business. Although Chinese mines continue to appreciate and value German mining technology, there is also a strong sense of wishing to use mining technology from their own country. Between these developments, the Chinese have also been working intensively for many years to gain information on the latest German technology and German expertise in the course of technical approval procedures.

Strong tendencies towards use of local equipment can also be observed in the Russian market. Russia is interested in German mining technology. However, many in the country are lamenting the fact that Russia’s raw materials industry is so dependent on imports and are therefore appealing to German companies to engage in more technological cooperation. The objective here is not only to achieve improvements in terms of health & safety at work and efficiency, but also to attract investment that can give a development boost to the country’s own industry – above all in terms of digitisation and automation.

In many other markets, particularly in Latin America and Africa, mines are being forced to close, as more and more people are becoming infected with coronavirus. In Australia, on the other hand, the “champagne corks are popping”, as recently reported in the press. Demand for gold and iron ore is strong and delivering Australian mining companies impressive profits.

The global consultancies consider the raw materials industry to be well-positioned in handling the crisis. However, both the rate of infection in the producing countries and developments in the customer sectors are leading to major uncertainties. Although these are clearly two different worlds with very different positions, they are both still suffering from the effects of the pandemic. There seems to be less demand for energy resources, which is therefore putting pressure on prices, e. g., since industries such as the automotive industry – and thereby also the steel industry – are operating at reduced output. Based on estimates of the consultants, raw materials with high demand, above all in China, are likely to be less susceptible to fluctuation and price changes. Indeed, the consultants expect the industry leaders among the mining companies to maintain their financial stability. On this basis, they will then, e. g., be able to work on the key factors of environmental, social and governance (ESG) or give greater priority to cyber security from the perspective of safety first. However, one common goal is to increase the general resilience to future crises beyond the scope of coronavirus and its effects. Digitisation has a key part to play here.

German mining suppliers are catering to these circumstances by driving “technology research” further forward. Digitisation represents a major part of this. However, other technical areas such as alternative drive concepts or further expansion of autonomous operations in mines are also affected. (VDMA/Si.)